Why operators keep getting this wrong

Table of Contents

A lot of sweepstakes game room owners still treat anti-money laundering like it belongs in somebody else’s office. The bank worries about it. The payment processor worries about it. Maybe the lawyer worries about it. Meanwhile the operator is focused on the floor, the software, the redemptions, the players, the endless little fires that eat up the day.

That is usually how the blind spot starts.

The room can look perfectly ordinary and still create financial risk. Credits are loaded. Credits are played. Prizes are redeemed. Staff handle transactions quickly because they do not want the counter backed up. A regular customer comes in, and nobody thinks twice. Then you look closer and realize the same account has a strange redemption pattern, or the same device keeps showing up under different names, or somebody is loading value and barely playing before cashing out. None of that sounds dramatic when it happens once. In a real operation, though, problems rarely arrive with a siren. They arrive disguised as routine.

That is where sweepstakes operators get themselves into trouble. They spend so much time asking whether the business fits a promotional model that they ignore a harder question: does the money flow inside the room make sense? If the answer is shaky, everything around it starts to wobble.

What AML means here, in plain terms

Forget the polished compliance language for a second. In a sweepstakes game room, AML is really about one thing: stopping the business from becoming a useful place to move questionable money.

That can happen in small, unremarkable ways. A player loads funds, does almost nothing with them, redeems, and comes back later to do the same thing. A cashier skips a check because the person is familiar. A payout gets processed without enough documentation because it is a busy afternoon and nobody wants an argument at the counter. An account profile looks incomplete, but the transaction goes through anyway.

This is why the casual answer “we’re not a casino” — does not solve much. It might be legally relevant in some contexts, but it does not make suspicious behavior disappear. Banks do not care about branding nearly as much as operators think they do. Payment partners do not care either. They care about how value moves. They care about whether the business looks controlled or sloppy. They care about whether somebody reviewing the records later can understand what happened without guessing.

That is why pages like Anti-Money Laundering, FinCEN MSB, and State Laws matter. Not because they sound official. Because operators need that context before they scale a system that has weak points built into it.

Where the real exposure usually sits

Most of the risk is not hidden in some advanced scheme. It sits right inside the basic workflow.

Cash loads are one pressure point. Manual prize payouts are another. So are inconsistent ID checks, weak cashier notes, missing redemption records, vague exception handling, and any setup where different kinds of credits start blurring together in practice. Operators tend to think of these as little operational details. Risk teams do not. To them, those details are the whole story.

The dual-currency model adds another layer. On paper it may be easy enough to explain: one set of credits for entertainment, another tied to promotional prize opportunities. But the moment redemptions enter the picture, people start asking questions. Who got what? What triggered the redemption? Was there meaningful gameplay? Was the activity documented? Could someone move value through the system without much friction?

Those questions matter because the room is being judged by more than regulators. It is being judged by processors, acquiring banks, fraud teams, sometimes by vendors who have no direct role in compliance but still have opinions about risk. An operator may think the system is functioning normally while everyone around them sees a room that looks undercontrolled.

That mismatch causes more damage than people realize.

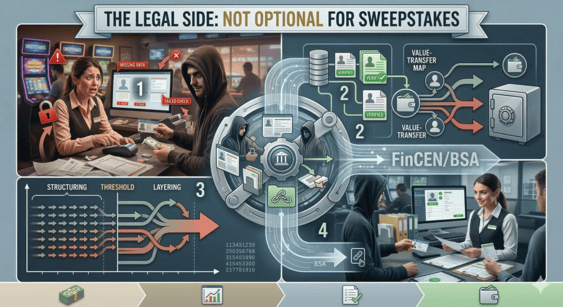

The legal side is not optional just because it is inconvenient

The U.S. framework around money laundering starts with the Bank Secrecy Act. FinCEN sits in that world and shapes how suspicious activity, reporting, and financial controls are treated. In the casino industry, that structure is familiar territory. Written AML programs, internal controls, reporting obligations, recordkeeping, review of unusual transactions — none of that is new.

Sweepstakes game rooms do not automatically fall into the exact same category, and that distinction matters. Still, this is where operators get lazy. They hear “not automatically” and turn it into “not my problem.” That shortcut is where bad assumptions multiply.

The real issue is function. If the business starts behaving like a place where value is stored, moved, redeemed, or routed in ways that look more financial than promotional, then MSB-related questions can start showing up. That is why Do Sweepstakes Operators Need an MSB License? and the site’s Legal Guide are worth connecting here. The concern is not what the homepage says. The concern is how the operation actually works when you strip the marketing language away.

Operators do not need to memorize every legal acronym, but they do need to understand the pressure points:

- large or unusual currency movement

- repeated or structured redemption activity

- thin or unreliable customer identification

- wallet or transfer features that start looking like money movement rather than simple promotion mechanics

If those pieces exist, ignoring them does not make them less important.

What a usable AML program actually looks like

A real AML program is not impressive because it sounds sophisticated. It is useful because people actually follow it.

That usually starts with a risk assessment. Not a generic one pulled from somewhere else. A real one tied to the room as it operates today. How are funds loaded? Where do redemptions happen? Who can override a payout? What gets logged? Which patterns would trigger review? Where are the weak spots if a player decided to test the system?

Once those questions are answered, controls start to make sense

| AML Control Area | What it should cover in a sweepstakes game room |

|---|---|

| Risk assessment | Payment methods, linked accounts, redemption patterns, repeat visits, shared devices, cash-heavy behavior |

| KYC / CDD | Identity checks, age checks, enhanced review for unusual or larger prize redemptions |

| Transaction monitoring | Quick load-and-redeem activity, split transactions, repeated same-day payouts, irregular player behavior |

| Suspicious activity logging | Internal notes, review steps, escalation history, reasons a case was flagged |

| Recordkeeping | Cashier logs, sales records, free entry records, prize payout documentation, exception notes |

| Training | Staff awareness, red flags, escalation lines, non-negotiable checks |

| Independent review | Periodic testing to see whether the process works outside of policy documents |

That may not look exciting, and honestly it should not. The strongest controls in this space are often the least glamorous. They are the ones staff understand, repeat, and do not quietly work around.

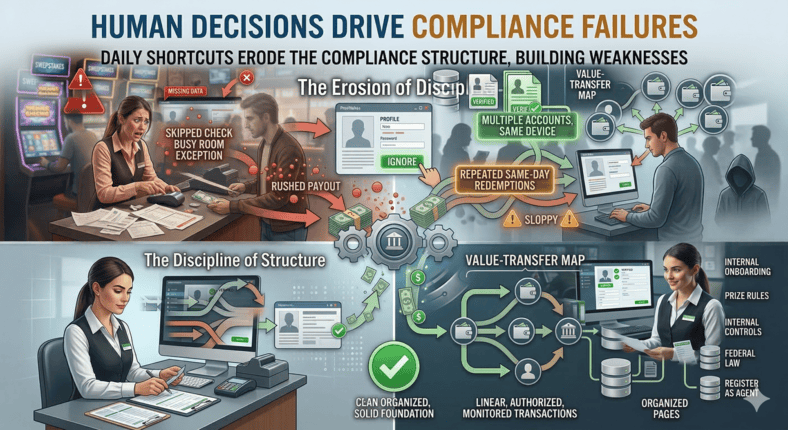

Most compliance failures are human, not technical

People love blaming software. Sometimes the software deserves it. A lot of the time, though, the real problem is habit.

An employee recognizes a player and skips the ID check. Someone makes an exception because the room is busy. A payout gets rushed through because there is a line forming. A profile has missing details, but nobody wants a confrontation. Each decision feels small enough to excuse. Stack enough of those together and the room develops a culture where rules are treated like suggestions.

That is where customer due diligence breaks down. Not through one spectacular failure. Through repetition. Through shortcuts becoming normal.

If prize redemption is part of the model, there need to be clear boundaries. Larger redemptions should trigger stronger review. Repeated same-day cash-outs should not blend into the background. Multiple accounts connected to the same device, address, card, or usage pattern should not be ignored just because the room is busy. Those are the places where discipline matters.

It also helps to connect that discipline to the rest of the compliance structure. Internal pages like No Purchase Necessary, Federal Law, and How to Register as a Sweepstakes Agent support the topic because AML does not sit in isolation. It overlaps with onboarding, documentation, prize rules, state law, and day-to-day operational controls.

A simple operator gut-check

Before an operator says, “We’ve got it covered,” a few questions are worth asking:

- Does the AML policy actually reflect how the room works in real life?

- Are redemptions, free entries, exceptions, and suspicious patterns documented properly?

- Do staff know when enhanced identification checks apply?

- Is anyone actively looking for quick load-and-redeem behavior?

- Has the room evaluated whether any wallet, payout, or transfer feature raises MSB concerns?

- Could the business explain its controls clearly to a processor, lawyer, bank, or examiner?

If the answers are vague, the weakness is probably not legal theory. It is the operation itself.