Table of Contents

From the outside, a sweepstakes platform can look deceptively simple. A few games, some promotional entries, prize drawings, maybe a leaderboard for engagement. Players log in, enjoy the entertainment, and occasionally win something. On the surface, it feels closer to a marketing promotion than anything complicated.

Spend a little time on the operational side of the industry, though, and the simplicity disappears quickly.

Behind almost every sweepstakes platform sits a web of overlapping rules. There’s promotional marketing law, gaming regulations, and—depending on how the platform handles payments—financial compliance rules as well. That overlap is exactly why one question keeps resurfacing among operators, distributors, and entrepreneurs exploring this space:

Do sweepstakes operators need an MSB license?

The answer rarely fits into a neat yes-or-no box.

Sometimes they do. Sometimes they don’t.

What determines the outcome isn’t the branding of the platform or the industry label it adopts. Regulators generally look past those surface descriptions. What they care about is the underlying mechanics: how the platform handles money, digital credits, and prize redemption.

Once you start examining those mechanics carefully, the regulatory picture becomes much clearer. Operators who want to build something durable—not just a short-lived gaming site—need to understand the line separating promotional sweepstakes gaming from regulated financial activity. Much of that line becomes clearer when reviewing compliance resources such as federal sweepstakes regulations, anti-money laundering compliance requirements, and the FinCEN MSB compliance framework that explains how financial regulators interpret money-service activity.

The rest of this discussion walks through that distinction—where the risks appear, why regulators sometimes look more closely at sweepstakes platforms, and how experienced operators design their systems with compliance in mind from the beginning.

Understanding Sweepstakes Gaming from a Legal Perspective

Sweepstakes gaming sits in a strange legal middle ground. It borrows some visual elements from gambling—chance-based outcomes and prize payouts—but legally it belongs to a different category: promotional marketing.

That difference rests on a very old legal concept. Under U.S. law, an illegal lottery normally contains three elements working together.

| Element | Meaning |

|---|---|

| Prize | Something valuable is awarded |

| Chance | Winners are determined randomly |

| Consideration | Players must pay to participate |

If all three elements are present at the same time, regulators typically treat the activity as gambling or an illegal lottery.

Sweepstakes promotions avoid that classification by removing one key ingredient: consideration. Participants must be able to enter the promotion without paying money. The Federal Trade Commission explains this clearly in its consumer guidance on sweepstakes and prize promotions.

That’s why legitimate promotions prominently display the familiar phrase “No Purchase Necessary.”

It isn’t just marketing language—it reflects a legal safeguard. Most sweepstakes platforms implement this through what’s known as an Alternative Method of Entry (AMOE), allowing someone to participate without buying anything.

Operators who want a deeper explanation of this structure often reference compliance discussions such as No Purchase Necessary sweepstakes rules and broader regulatory explanations in the site’s legal guide.

Still, sweepstakes legality alone doesn’t resolve every compliance question. As soon as a platform begins managing digital credits, stored balances, or prize redemption systems, regulators may begin examining whether those mechanics resemble financial services. That is where the conversation about MSB licensing begins to appear

What Is an MSB License?

The term MSB stands for Money Services Business, a classification defined under the Bank Secrecy Act. These businesses handle certain financial activities involving the movement or exchange of money.

According to guidance published by the U.S. Treasury’s Financial Crimes Enforcement Network, a money services business may include entities engaged in functions such as money transmission, currency exchange, check cashing, or prepaid value issuance. The agency’s explanation of money services business regulations outlines how these businesses must register and maintain compliance programs designed to prevent financial crime.

Once a company falls into the MSB category, federal law expects it to implement systems that detect suspicious financial activity.

Those safeguards typically include:

- Anti-Money Laundering (AML) monitoring

- identity verification procedures

- suspicious activity reporting

- financial recordkeeping requirements

The IRS also provides an overview of these obligations in its MSB compliance information center.

One point becomes clear when reading these regulatory explanations: a business becomes an MSB because of the financial services it performs, not because of the industry it claims to belong to.

That distinction is crucial when evaluating sweepstakes gaming platforms.

Why Sweepstakes Platforms Trigger MSB Questions

Traditional sweepstakes promotions rarely resemble financial systems. A participant submits an entry, perhaps fills out a form, and occasionally wins a prize. The process begins and ends within the boundaries of a promotional contest.

Modern sweepstakes gaming platforms often operate differently.

Many platforms now rely on dual-currency models that separate entertainment gameplay from promotional rewards.

| Currency Type | Purpose |

|---|---|

| Gameplay credits | Used for entertainment play |

| Sweepstakes credits | Sometimes redeemable for prizes |

From a design perspective, the model works well. Players enjoy gameplay using entertainment credits while promotional credits determine prize eligibility.

But this structure also introduces a regulatory gray area.

If players are able to purchase credits, maintain balances in an account, redeem promotional currency, or receive cash prizes, regulators may begin asking whether the system resembles a financial value-transfer mechanism.

FinCEN’s interpretation of money transmission regulations focuses on the acceptance and transfer of value between individuals. When digital credits begin functioning as stored value, the regulatory conversation can shift toward financial compliance.

That doesn’t automatically mean a sweepstakes platform is operating illegally. But it does mean regulators may examine the structure more carefully.

When Sweepstakes Operators May Need MSB Registration

Sweepstakes operators generally encounter MSB analysis when their platform starts performing activities similar to a financial intermediary.

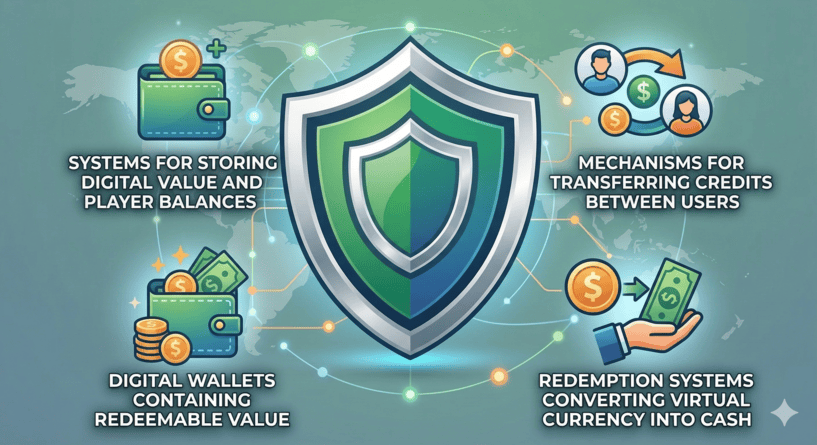

Common examples regulators evaluate include:

- systems that store player balances

- mechanisms that transfer credits between users

- digital wallets containing redeemable value

- redemption systems converting virtual currency into cash

When these elements appear together, authorities may evaluate whether the platform qualifies as a money transmitter under FinCEN rules.

The agency’s advisory on money transmission compliance explains that businesses transferring value between persons may fall within MSB classification.

For sweepstakes operators, the most sensitive point often involves how promotional currency is redeemed. If credits can be converted into real money or monetary equivalents, regulators may analyze whether the system behaves like a financial mechanism.

That analysis doesn’t automatically classify the platform as illegal—but it does make compliance planning significantly more important.

State Laws Also Shape Sweepstakes Compliance

Federal financial regulation is only one layer of the compliance picture. Sweepstakes operators must also navigate state-specific promotional laws.

Certain states impose registration requirements for large promotional contests.

| State | Requirement |

|---|---|

| New York | Registration for prizes above $5,000 |

| Florida | Registration and bonding requirements |

| Rhode Island | Retail promotion registration |

New York’s games of chance registration guidelines provide an example of how these rules work.

Because requirements vary by jurisdiction, operators often review state-specific compliance discussions when evaluating risk. Helpful resources include:

- Virginia sweepstakes legal framework

- Georgia sweepstakes gaming laws

- Michigan sweepstakes machine laws

- South Carolina game room legal framework

Understanding both federal and state regulations helps operators avoid unpleasant surprises later.

AML Compliance: The Overlooked Risk for Sweepstakes Platforms

One of the most common compliance mistakes sweepstakes operators make is focusing entirely on gaming legality while overlooking financial crime prevention rules.

The Bank Secrecy Act, explained by the IRS in its overview of BSA compliance requirements, requires financial institutions to maintain systems capable of identifying suspicious financial activity.

Those systems typically involve:

- transaction monitoring

- identity verification

- reporting suspicious transactions

Why does that matter for sweepstakes operators?

Because when a platform begins handling financial value—even indirectly—regulators may expect basic safeguards against misuse.

Without those safeguards, a system could potentially be exploited for:

- money laundering

- fraud schemes

- financial manipulation

That’s why experienced operators spend time studying compliance topics such as skill-based gaming law and regulation and broader regulatory frameworks before launching large-scale gaming platforms.

Designing Sweepstakes Platforms the Smart Way

Entrepreneurs entering the industry often focus heavily on software, graphics, and game distribution. Those elements matter, of course, but the most sustainable platforms pay equal attention to their compliance architecture.

That architecture usually includes:

- clear promotional rules

- a properly implemented AMOE system

- documented prize redemption procedures

- payment monitoring policies

- periodic legal review of platform mechanics

Operators interested in distribution models can also study operational strategies described in how to become a sweepstakes game distributor and how to register as a sweepstakes agent.

Platforms built on strong compliance foundations tend to last longer—and attract fewer unpleasant surprises from regulators.